“He will win whose army is animated by the same spirit throughout all its ranks.”

Sun Tzu, The Art of War

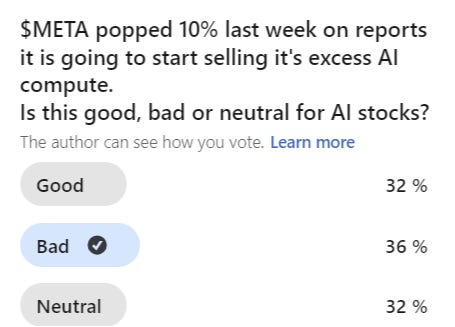

In my latest poll I asked if $META’s pop of 10% on reports that they would start selling excess AI capacity was good, bad or neutral for the AI narrative. Bad slightly edged it but broadly it was evenly split between the 3 views.

This is incredibly interesting. It flies in the face of the efficient market hypothesis for one (if that’s still a thing people believe in). It also revealed how we look at singular important events through different lens’. Several of those who responded also emailed me to express their views and there was one respondent who put their thoughts in the comments and across all responses there was a spread of thinking.

If I can summarise, the high level arguments are:

GOOD: It is more capacity for AI, signifies growth, promotes wider adoption and is a sign of a maturing sector.

BAD: META 0.00%↑ overbuilt for AI demand and is now repositioning to limit losses potentially signalling a broader repositioning as AI Hyperscalers struggle to generate the returns on investment for the massive capex outlays. Cheaper Asian offerings and reports of token costs exceeding the engineers replaced support the view.

NEUTRAL: Meh. More of the same.

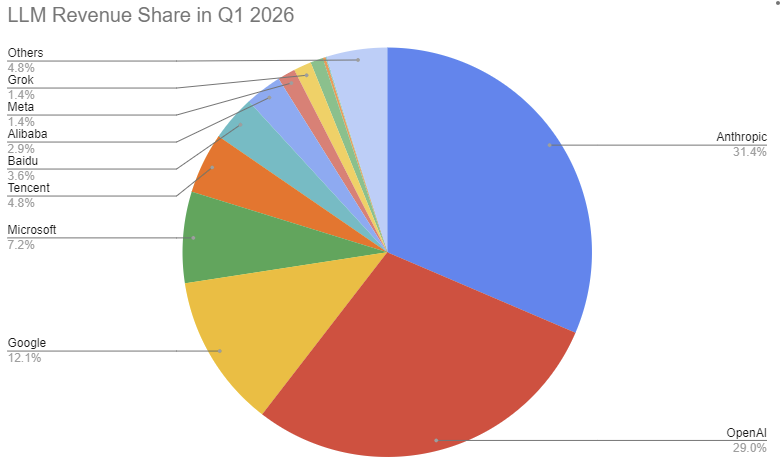

My own view is that it is BAD for the story but could be great for one of the players. To me this shows a levelling out of demand and the herd being culled. Those hyperscalers who have seen little take up in demand and are clearly not in the race are starting to hedge their exposure. Meta and xAI are the two operators who have begun to sell their excess compute and they account for just over 1% each per below.

LLM Revenue Share Q1 2026

Source: Counterpoint Research, April 2026

META 0.00%↑ it should be noted are still reeling from the metaverse fiasco which had reduced the stock price to $89 and consumed over $80bn of capex. AI guidance for 2026 is $120bn - $145bn. It’s no surprise that they are one of the first to flinch. Grok have also indicated they would be selling compute capacity albeit they framed it as having an excess of build rather than insufficient demand. Neither Meta’s Llama and xAIs Grok have broken through on market share and as such, like a political race, are bowing out to others and rightfully so.

This is where things get interesting. Until now the question was whether AI would succeed but now the question itself is bifurcating into whose AI will succeed and is that worth anything. This is shakier ground for the broader narrative that markets have been moving on and for which IPO’s are being positioned for. Meta is relatively insulated because of its major cash generation and Grok is also insulated behind the SpaceX and Starlink shields (see previous piece SpaceX: Musk vs reasonable stock valuations here) albeit this should under normal circumstances impact the SPCX 0.00%↑ narrative but that’s not a normal price setting. This leaves - of the companies on extended valuations - MSFT 0.00%↑ ,GOOGL 0.00%↑ , Open AI and Anthropic. As competition bows out it leaves fewer to share the spoils. My feeling is that, based on unit economics there is more bowing out to happen but my current thoughts are as follows: