“The supreme art of war is to subdue the enemy without fighting.”

Sun Tzu, The Art of War

Note: None of the material or content contained herein constitutes investment advice. It is solely for educational and informational purposes. Past performance is not an indicator of future performance.

In 2017, I was at my desk watching the Tesla story play out in real time. I was following analysis and opinion closely, industry analysts, fintwit analysts, office analysts. My own analysis clearly pointed to the collapse of the company at any moment. Missed guidance, shambolic production, a litany of broken promises, troves of service horror stories, high capex burn, a lack of supporting infrastructure etc. I waxed lyrical to colleagues about the imminent demise of Tesla. But, I was completely wrong. It soared to levels that were greatly disconnected from fundamentals and appropriate risk tolerances. Today it sits at $420, the eponymous 2funding secured figure. It has a market cap greater than all the other major car companies combined and commands a market cap over 14x that of peer BYD, who sell nearly 25% more EV’s than Tesla.

The Tesla experience was a vital one for me and my investment philosophy. Every now and then prices will develop in a stock or stocks that can’t be justified by optimistic fundamentals - or even visionary ones, but equally, being deadly sure that it can’t possibly last - let alone grow in value is naïve.

On June 12th, SpaceX is set to IPO in a record breaking and controversial float. It is a story of risk, genius, innovation, science fiction and above all, money.

The SpaceX story is fascinating and will undoubtedly be required reading on finance courses in the near future. It is likely to be the most valuable IPO in history by a wide margin ($2T vs Saudi Aramco in 2019 for $1.7T). Before we outline why this fits the bill for the Sun Tzu quote - The supreme art of war is to subdue the enemy without fighting - we have to step back and understand the background to SpaceX.

🏗️ 2002: The Founding

Musk funded the inception and early development of SpaceX entirely himself with roughly $100 million of his own capital, which he had earned from the sale of PayPal to eBay.

During its first few years, SpaceX operated independently, aiming to prove that a small, vertically integrated team could build a cheaper, reusable rocket from scratch.

The stated, long-term goal was to make humanity multi-planetary and colonize Mars, but the immediate business problem was that traditional aerospace contractors were too expensive and moved too slowly.

🚀 2008: Orbit and Survival

By 2008, SpaceX had attempted to launch its small Falcon 1 rocket three times. All three launches had failed, and Musk was virtually out of money. Everything inged on the fourth launch succeeding in September 2008. Failure and the endeavour was over or success and the dream could continue. Thankfully, it was a success and on the back of that success and SpaceX’s participation in NASA’s Commercial Orbital Transportation Services development program, NASA awarded SpaceX a $1.6 billion Commercial Resupply Services contract in December 2008 to fly cargo to the International Space Station, effectively saving SpaceX and providing the capital to develop larger rockets.

📉 2015: The Economics Shift

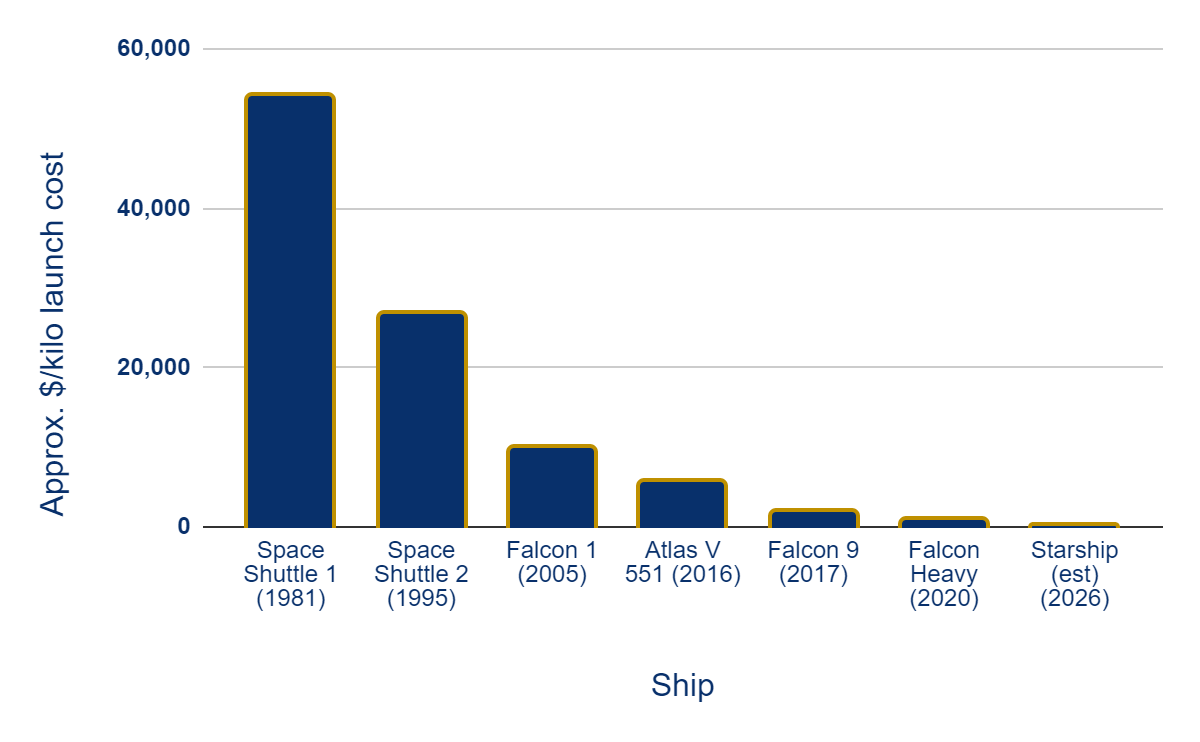

7 years later in 2015, SpaceX fundamentally altered the economics of spaceflight by successfully landing the first stage of a Falcon 9 orbital rocket back on Earth. And it can’t be denied, when the light clears and we see the first stage standing upright it is a truly inspiring moment, a true leap forward for space exploration. By proving that orbital-class boosters could be recovered and reflown, rather than discarded into the ocean, SpaceX began driving launch costs down to a fraction of the competitors’. For example, since 1981 with the Space Shuttle to 2026 with SpaceX Starship, the cost of getting a kilogram to space will have fallen by a factor of over 200x, from $54k per kilo in 1981 with the Space Shuttle to c.$200 per kilo for Starship.

Historic cost of getting a kilogram to space

Source: https://www.visualcapitalist.com/the-cost-of-space-flight/

The cost of getting freight to space via SpaceX is now so low it can best be demonstrated by the space selfie. CrunchLabs sent a satellite into space on a SpaceX rocket for the sole purpose of allowing people to get their selfie taken in space - you can check it out here. This is truly an incredible leap in economic accessibility and SpaceX and Musk can be entirely credited with that.

🛰️2019: The Connectivity Network

On the back of the successful launch program, SpaceX launched the first operational batch of Starlink satellites into Low Earth Orbit, beginning the assembly of a mega-constellation designed to provide low-latency, high bandwidth, broadband anywhere in the world. It could even be achieved on Ryanair flights if needed but not at a cost O’Leary would tolerate.

Starlink has not been without serious concerns either - e.g. Musks influence over war zones but it has proven to be a highly profitable business.

The following year, SpaceX’s Crew Dragon spacecraft successfully carried NASA astronauts to the International Space Station, ending a nearly decade-long US reliance on Russian Soyuz rockets for crew transport.

💪 2024: Market Dominance

By 2024, SpaceX was routinely flying refurbished Falcon 9s and executing over 130 launches a year taking Starlink satellites to space along with paid slots for other companies, capturing more than 50% of the global commercial launch market. Meanwhile, the fully reusable, super-heavy-lift Starship vehicle began hitting major developmental milestones, paving the way for much heavier payloads and lunar missions. Starship will truly be a breakthrough for humanity. It is expected to be able to carry over 100 metric tonnes into space - this is important for delivery the parts needed for larger scale structures such as lunar bases, datacentres in space and the colony on Mars, Musk has dreamed of.

🤖 2026: The AI Pivot

In February 2026 the story changed however, SpaceX acquired xAI, Musk’s AI venture - more commonly known as Grok. The messaging around the combining of these businesses suggested SpaceX was no longer just a space operations company but was now going to be an artificial intelligence and orbital computing infrastructure business. The move added complexity to the vision and muddied the clear story of SpaceX but it also boosted the valuation. Some say the motivation was for a vision like never before, AI and Space under one roof but others are concerned it is a convenient way to shield the capex hungry and less attractive xAI story behind the strength of the SpaceX story.

This is where Musk is subduing the enemy without fighting.

People associate SpaceX with launch services - in which they have a monopoly. Starlink and xAI however, are most certainly not monopolies. Starlink is profitable with a good future ahead of it but faces competition from domestic telecoms and data networks. xAI is in a land war with Anthropic, OpenAI, Google, Meta and a host of Chinese AI models and only a few will survive when the dust has settled. It is also devouring capital and revenue growth is patchy at best. By putting xAI into SpaceX that story has been shifted and is no longer part of the hyperscaler land war conversation but now part of the inspiring sci-fi story. Bold visions sell stocks and Musk knows this. But what of the numbers? Let’s look at the basic headline figures.

Estimated valuation of SpaceX (launch services + Starlink + xAI) on IPO - $2trillion

Based on these numbers and accounting for the rate of growth currently being experienced, it would take 11.5 years for REVENUES to reach $2 trillion, let alone profits. That’s also assuming that growth momentum continues at the current pace which it rarely does. It is one of the more stretched valuations you will find, going well beyond the “priced to perfection” label that is often associated with such valuations. I would go as far as to say that the valuation of $2T is a nonsense compared to fundamentals but that is not to say it will not hold its value or even grow.

As I learned through my Tesla experience and as was discussed in our recent Boom and Bust conversation with John Turner and William Quinn, these dynamics occur with some regularity.

THE MUSK EFFECT

The Musk premium is an important factor. The combination of the great vision laid out, his previous achievements in innovation, his cult-like following and his history of delivering incredible stock performance against all odds are all in play. Maybe not as brightly as was with Tesla or maybe there is a new guard of devotees minted in the last few years who can send SpaceX stock - to the moon.

NAUGHTY NASDAQ

A second factor, which has been a controversial one is how Nasdaq have altered the rules to include SpaceX into the Nasdaq-100. They changed three major rules to win the SpaceX listing and they are worth understanding because structurally they enhance the probability of SpaceX performing.

SEASONING - Historically, companies were required to trade publicly for three to 12 months before they were eligible to be added to the Nasdaq-100. This “seasoning” period existed to allow the market to discover the stock’s true price before passive index funds were forced to buy it but for SpaceX, Nasdaq introduced a “Fast Entry” rule that allows megacap stocks to be added to the index just 15 trading days after their IPO. The consequence is that there is a 15 day window of free price action - not typically enough to find a proper level - before the passive tap is switched on and the wave of passive flows bouy and boost the price.

FREE-FLOAT - Nasdaq eliminated the rule requiring a minimum 10% free float for index inclusion, clearing the way for companies with massive valuations but tightly held ownership to join immediately. Because SpaceX is expected to float only about 5% of its total equity at listing, it would have failed Nasdaq’s previous requirements. Only having 5% of your shares setting the price is a structural advantage as that 5% sets the price for whole 100%, largely held by Musk. If the buyers of the 5% are predominantly fanboys who are not interested in fundamentals and passive funds then the level is likely to be distorted upward.

INDEX WEIGHTING - The Nasdaq-100 has been until now a market-cap-weighted index but if they included SpaceX, with only 5% of shares of a $2T market cap available to buy, this would cause a host of problems. As passive indexes buy shares to try replicate the index they would be driving demand for the shares through the roof as there would not be enough shares for them all to fulfil their allocations. To mitigate this, Nasdaq introduced a rule that if the available amount of shares is less than 33% of the total shares in a company, the market cap would be 3x the valuation of the listed shares valuation (i.e. 5% x 3). It could still cause some issues and will need to be watched.

WINDOW of ACCOUNTABILITY

Another advantage to Musk and the stock price is the inherent timeline to Space. 11.5 years (for revenues to reach valuation) isn’t a long time when it comes to space, things take time - even SpaceX will take time to get things done. This dynamic works to the advantage of lofty valuations and promises of them delivering science fiction like outcomes in the future. If the valuation ultimately gets accepted by the market - which is likely due to the gaming of the Nasdaq rules, then Musk has vastly wider time horizons to keep the story spinning than he did with Tesla, where, for example, missed visions of autonomous vehicles and cybertrucks could only be excused for so many quarters.

CONCLUSION

In conclusion, the valuation is a nonsense. That rules me out of buying it. But I would also not short it. The structural elements at play mean this IPO has been engineered to maximise upside and minimise downside. In addition, the exuberance from those who idolise Musk and believe wholeheartedly in his ability to deliver science fiction in a matter of years will keep the stock elevated. I believe that it is very probable that the SpaceX stock price defies gravity and goes ad astra. But I won’t be onboard.

Agree with you on this one - it'll be one part share, one part Bitcoin. And if Bitcoin can got to $100k, there's no telling what this can do.