Can UK exceptionalism still deliver returns for investors?

- Financial Times Headline, 2038

Note: None of the material or content contained herein constitutes investment advice. It is solely for educational and informational purposes.

Yesterday, I was lucky to attend the Scottish Boutiques session in the Guildhall. It was a busy afternoon with many in the audience from across the industry. The venue was a surprising gem. Through a courtyard and gallery to a stunning ante room for presentations.

Scotland is arguably the cradle of modern finance and this spirit was firmly on display yesterday.

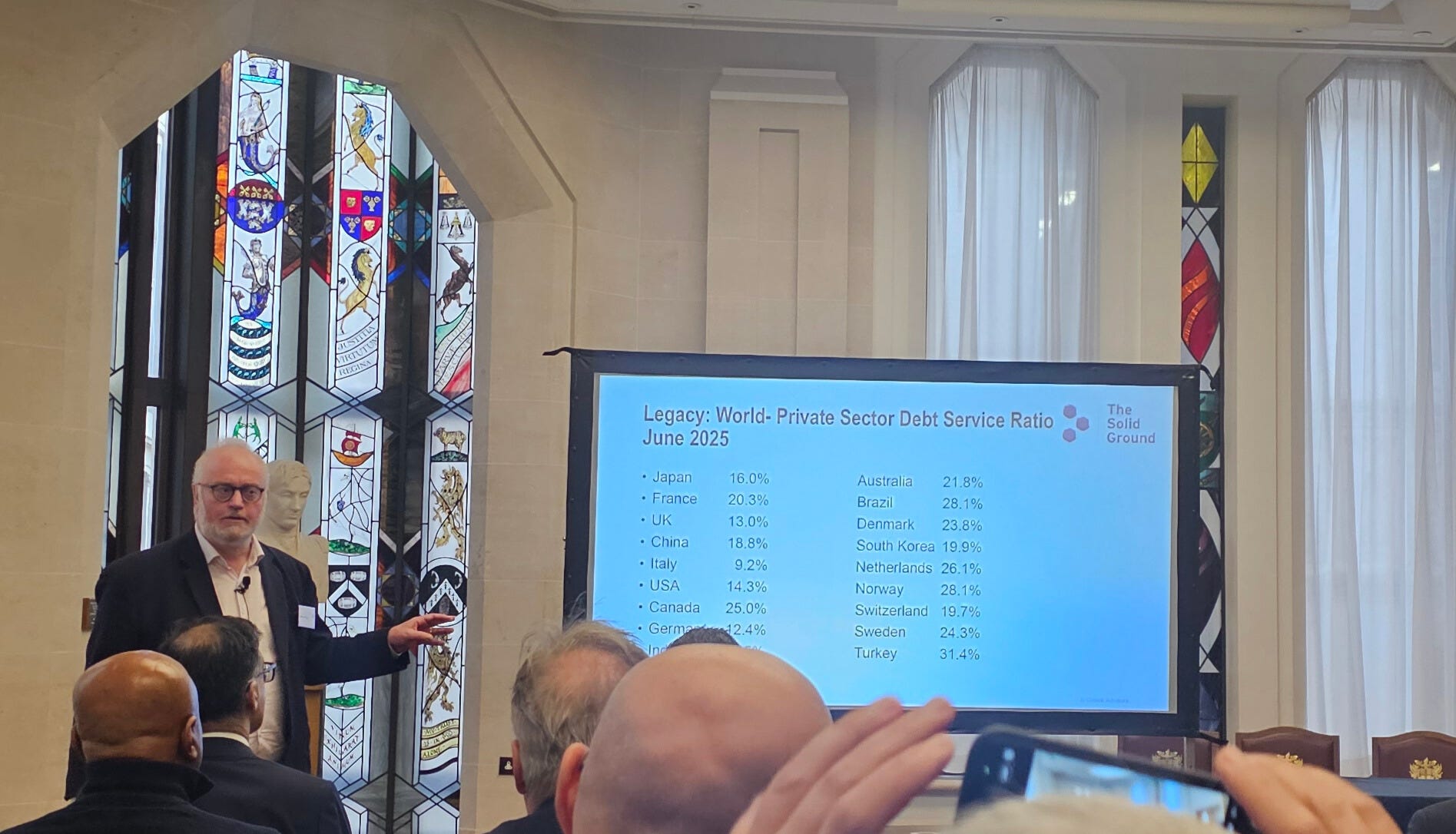

Russell Napier

The session began with a macro intro from Russell Napier, Keeper of the Library of Mistakes and author of The Solid Ground newsletter.

Russell laid out a convincing argument for the end of the investment world as we know it and highlighted that there is no such thing as exceptionalism over the longer term. He cited several dynamics: US total debt (not just government debt) as a % of GDP was c.100% at the beginning of the 80’s but has since climbed to c.250% today. Not only is this unsustainable but 70% of the world’s invested assets are sitting in the middle of it he notes. He expects that a combination of diversification and pull back from an increasingly volatile landscape could be the market equivalent of Napoleons retreat from Moscow. Long, slow and bloody. He also noted that of the few routes out of this situation, inflation is the most historically likely, thus US bonds which make up a huge portion of global AUM are likely to suffer.

He concluded that, in his view, over the next decade or two, value equities such as the UK and Japan as well as India are the places to be. Taking a leaf out of Citrini’s recent report, he looks forward to this time next decade when the headlines read, “Can UK exceptionalism still deliver returns for investors?”.

Mikhail Zverev, Amati Global innovation fund

Next, Mikhail Zverev of the Amati Global Innovation Fund (our next Expert-in-Conversation guest - details here) outlined how they invest in innovation, specifically though that they invest in businesses, not science projects.

Relatively young as a fund they’ve been finding traction in their approach of avoiding the herd but getting out there, to the trade shows and into the weeds of the innovation they are exploring. Whether it’s the annual conference on radio pharma, multinomics, industrial software or defence, the Amati team is likely to be there. They also highlight that of the list of major global innovation funds they have almost no overlap in exposures with others.

David Keir, Dundas Global Investors

David Keir was up next. Managing Partner of Dundas Global Investors and PM on the Heriot Global Fund, he talked about love letters.

I can feel you close to me, even though you’re far away.

Please believe me when I say I love you

Annual dividend declarations he said, were akin to love letters (like that above) from companies to their shareholders.

He outlined a strategy that has fallen out of the zeitgeist but remains en vogue when it comes to being a research supported approach - dividend growth.

He outlined several pieces of research (e.g. MSCI report) that highlight that the bulk of gains for markets over 10 year periods can be explained by company dividend strategies and performance. He gave examples of how dividend strategies that perform tend to lead to stock prices that perform. Dividends tend to enforce capital discipline, they’re real and they highlight a love of the minority shareholder.

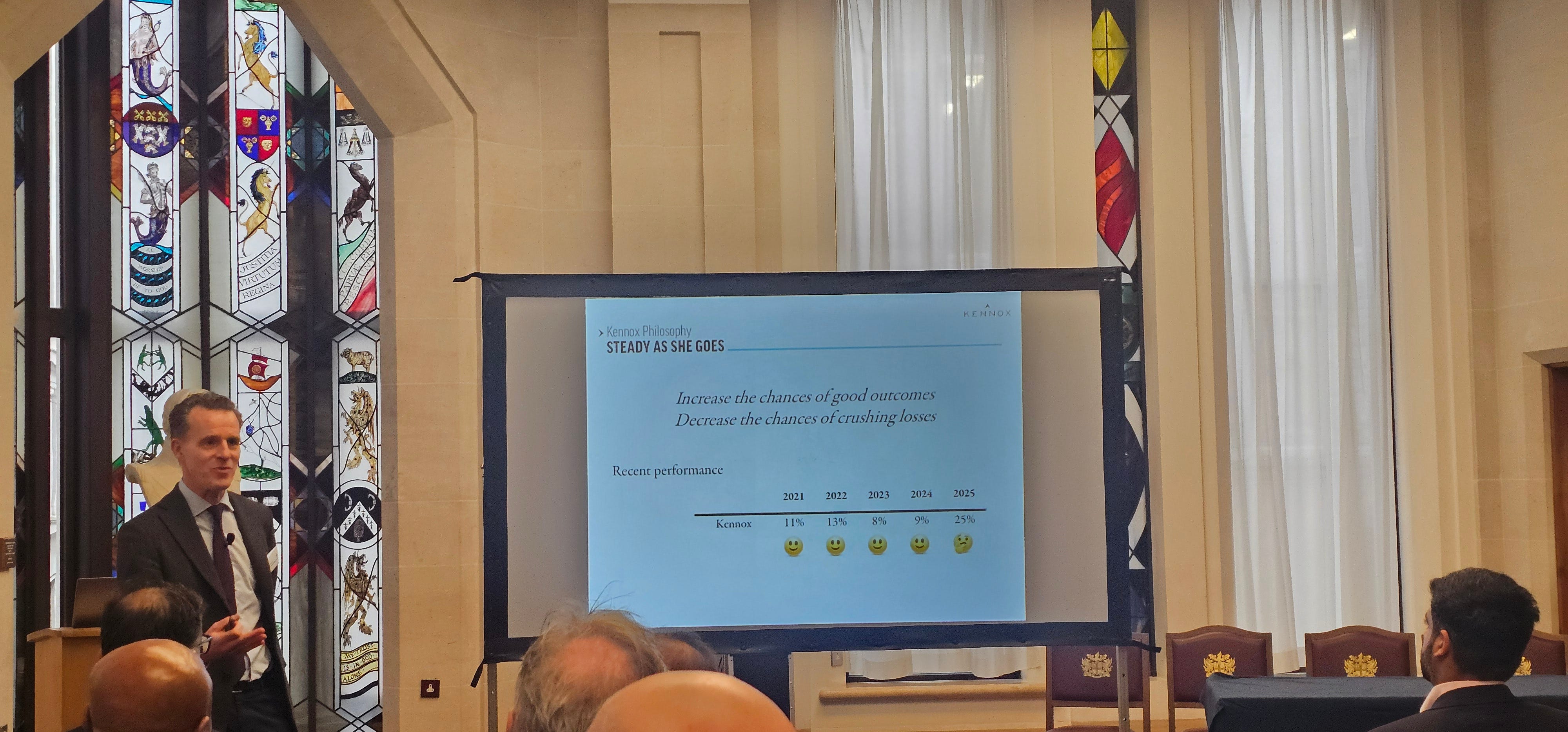

Charles Heenan, Kennox Asset Management

Charles Heenan of Kennox Asset Management was next.

He outlined the resurgence in value investing on the back of a riskier world. He made the case that the aim of investing is to increase your chances of good outcomes while decreasing your chances of crushing losses which value is well placed to achieve. He also outlined the heightened risk environment in global markets and how the approach at Kennox sits apart from the likelier trouble spots. They only have 2 names in the US for example, while finding plenty of opportunities in the UK, Europe, South East Asia and Australasia - a nice complement to prevailing core equity portfolios. One name he referenced as an under the radar opportunity they identified several years ago is Youngone Holdings. A lesser known Korean apparel company producing a range of clothing and items for international brands such as Patagonia and The North Face. As recently as 2022 it was trading at c.1x earnings, even as earnings continued to grow. The stock has expanded by 4x in 4 years but it still sits in value territory according to Heenan.

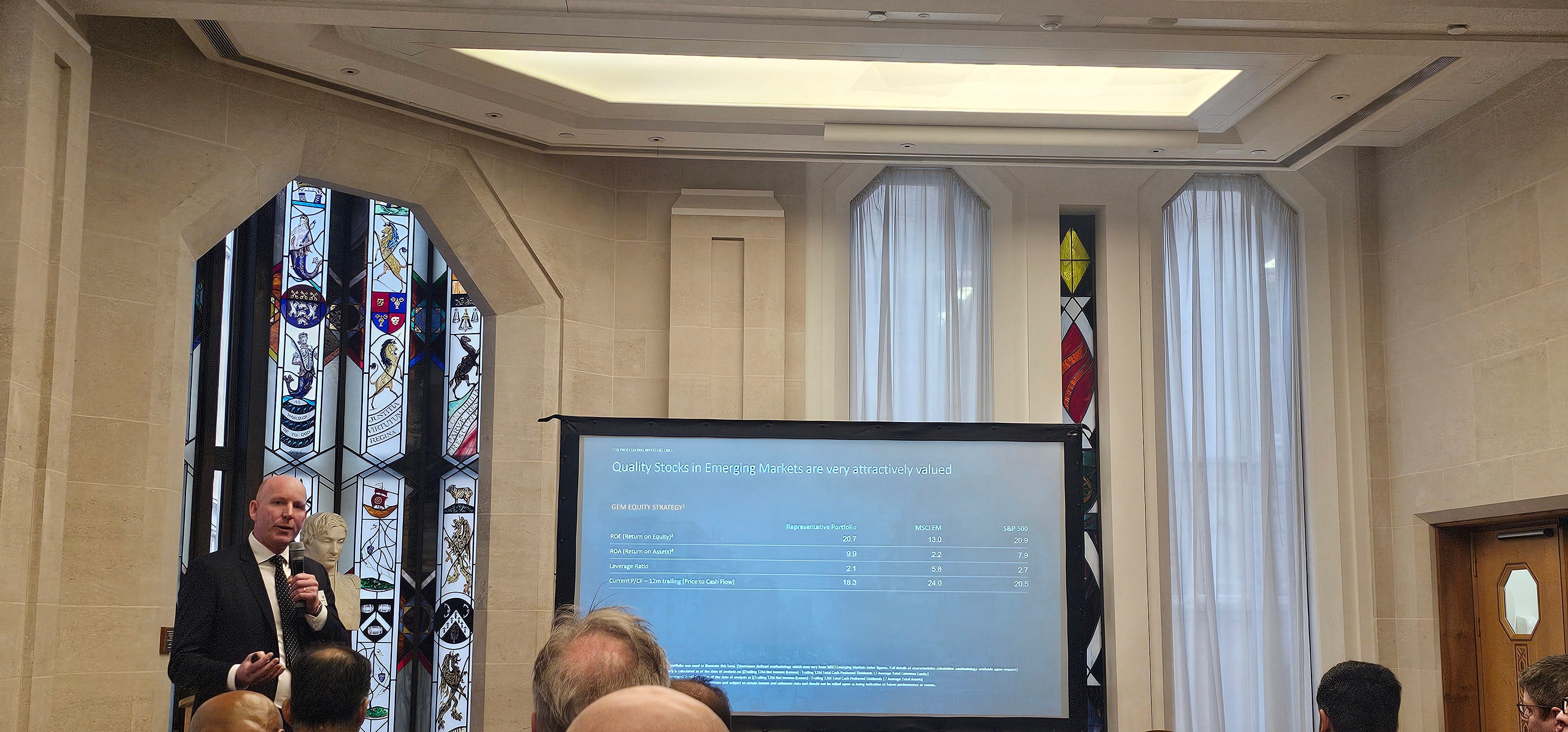

Glen Finegan and Cecilia Bosman, Skerryvore Asset Management

The final presentation of the day fell to Skerryvore Asset Management, the Emerging Markets asset manager based in Edinburgh.

Named for the Skerryvore lighthouse, in the wild seas of the Hebrides, resolute, guiding the less informed or less experienced to safety. This was a two part presentation, with Glen Finnegan, lead PM and founder of the fund, first outlining the 3 g’s of investing in emerging markets, governance, governance and governance. You are unlikely to see it from the government in these markets so it must be present and strong within the companies he says. It can be found though and often, in emerging markets, behind a strong governance policy lie very attractive opportunities. Glen then passed the mic to Cecilia Bosman.

Cecilia is a young analyst in the team who presented impressively, outlining two case studies of Skerryvore’s approach, Raia Drogasil in Brazil and Midea, the Chinese white goods and electronics firm. For Midea, she highlighted how the company respects minority shareholders, is sitting on a history of innovation, $12bn in net cash and equivalents, a P/E of 13, P/FCF of 12%, a dividend yield of 4.6%, the tailwind of South East Asia growth and the optionality of a resurgent Chinese property sector. A compelling conclusion to the formal presentations.

A lively Q&A followed with discussions ranging from where the industry might go in 5 years to innovation and demographics in emerging and frontier markets to what were each of their biggest mistakes and subsequent learnings.

Other notes and quotes:

The most money I’ve made in my life has come from investing in assets people have laughed at me for - Russell Napier, The Strong Ground

You have to be concerned about US assets, foreign investors own 210% of GDP - Russell Napier, The Strong Ground

Dividend notices are like love letters to investors and they’re real, research backed and drive capital discipline. You should get worried when they stop coming. - David Keir, Dundas Global Investors

UK is out of favour, so we’re interested - Charles Heenan, Kennox Value Fund

There were times we were lucky to get out of the meeting alive - Glen Finegan, Skerryvore AM, on governance meetings in emerging markets

Couple of hundred billion here and couple of hundred billion there and you soon start to talk about real money - Russell Napier on asset flows out of US

A great day, thank you to all who organised and it was wonderful to see Scotland and it’s investment heritage represented so well.

copyright BREAKINGWATERS Media ltd