Note: None of the material or content contained herein constitutes investment advice. It is solely for educational and informational purposes. Past performance is not an indicator of future performance. Sources: Fiscal.ai, Google Finance, 23 May 2026.

THE VIDEO BRIEF

THE AUDIO BRIEF

THE RUNDOWN

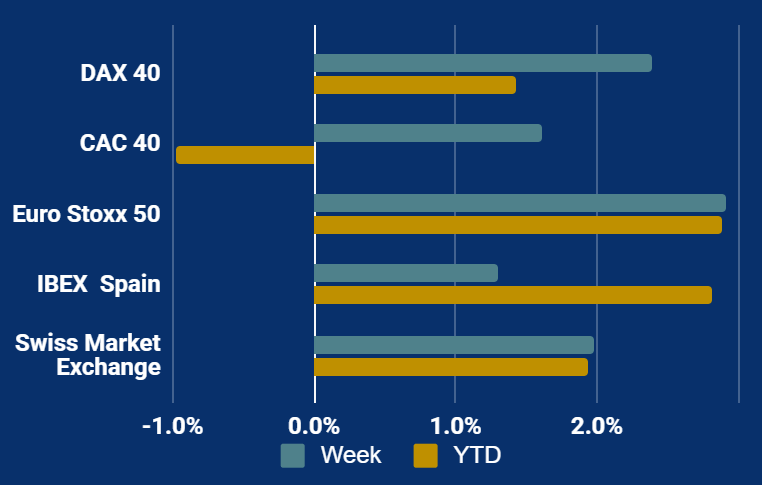

European markets trended higher this week as optimism grew regarding potential US-Iran peace talks and a de-escalation of Middle East tensions. The Euro Stoxx 50 led with a 2.9% gain, buoyed by a strong rotation into AI-related tech stocks like ASML and Nokia.

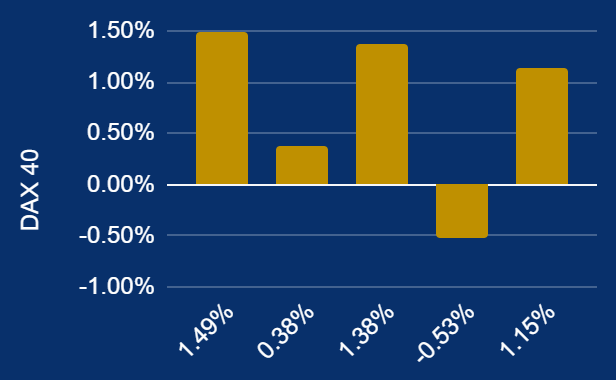

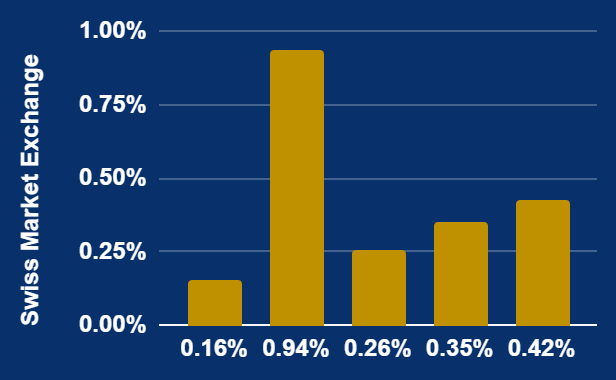

Germany’s DAX 40 rose 2.4%, supported by positive domestic business climate data and industrial strength, while the Swiss Market Exchange gained 2.0% due to solid luxury sector earnings, notably from Richemont.

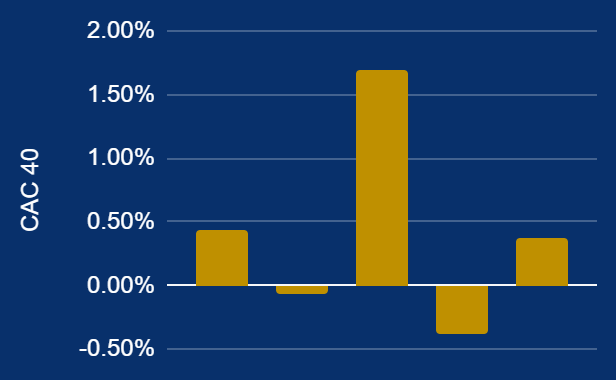

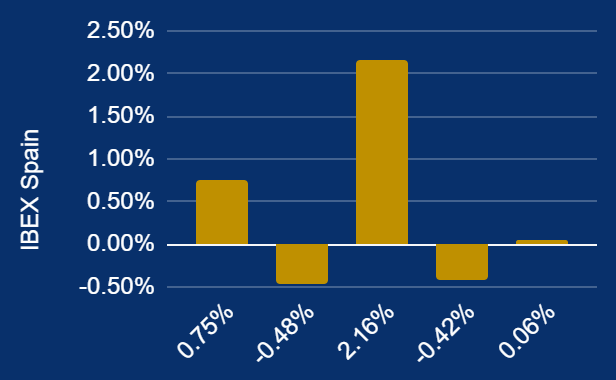

The CAC 40 increased 1.6%, though it lagged slightly as concerns over high-end consumer demand and regional inflation persisted. Spain’s IBEX 35 rose 1.3%, trailing peers as broader economic uncertainty and energy price fluctuations weighed on the domestic outlook.

Overall, while geopolitical risks remain, markets benefited from a pullback in bond yields and hopes for a reopening of the Strait of Hormuz.

MOVERS AND SHAKERS

RISERS

ASML Holding (ASML NA) manufactures chipmaking equipment and fell up to 7.1% due to new US export controls and geopolitical uncertainty regarding sales to China.

Infineon Technologies (IFX GY) produces semiconductors and fell as part of a 1.6% drop in the DAX 40 amid regional geopolitical tensions and inflation fears.

Ferrari (RACE IM) produces luxury performance cars and its stock dropped over 16% this month following suspended deliveries due to conflict in the Middle East.

FALLERS

Munich Re (MUV2.DE) is a global reinsurer whose shares fell 3.06% following Q1 investment-related headwinds and market volatility impacting its fixed income portfolio.

Eni (ENI.MI) is an integrated energy company that fell 2.92% amid general market movements and geopolitical tensions affecting global oil price stability.

Ahold Delhaize (AD.AS) is a retail supermarket group that declined 2.60% due to concerns over inflation and falling consumer sentiment impacting purchasing power.

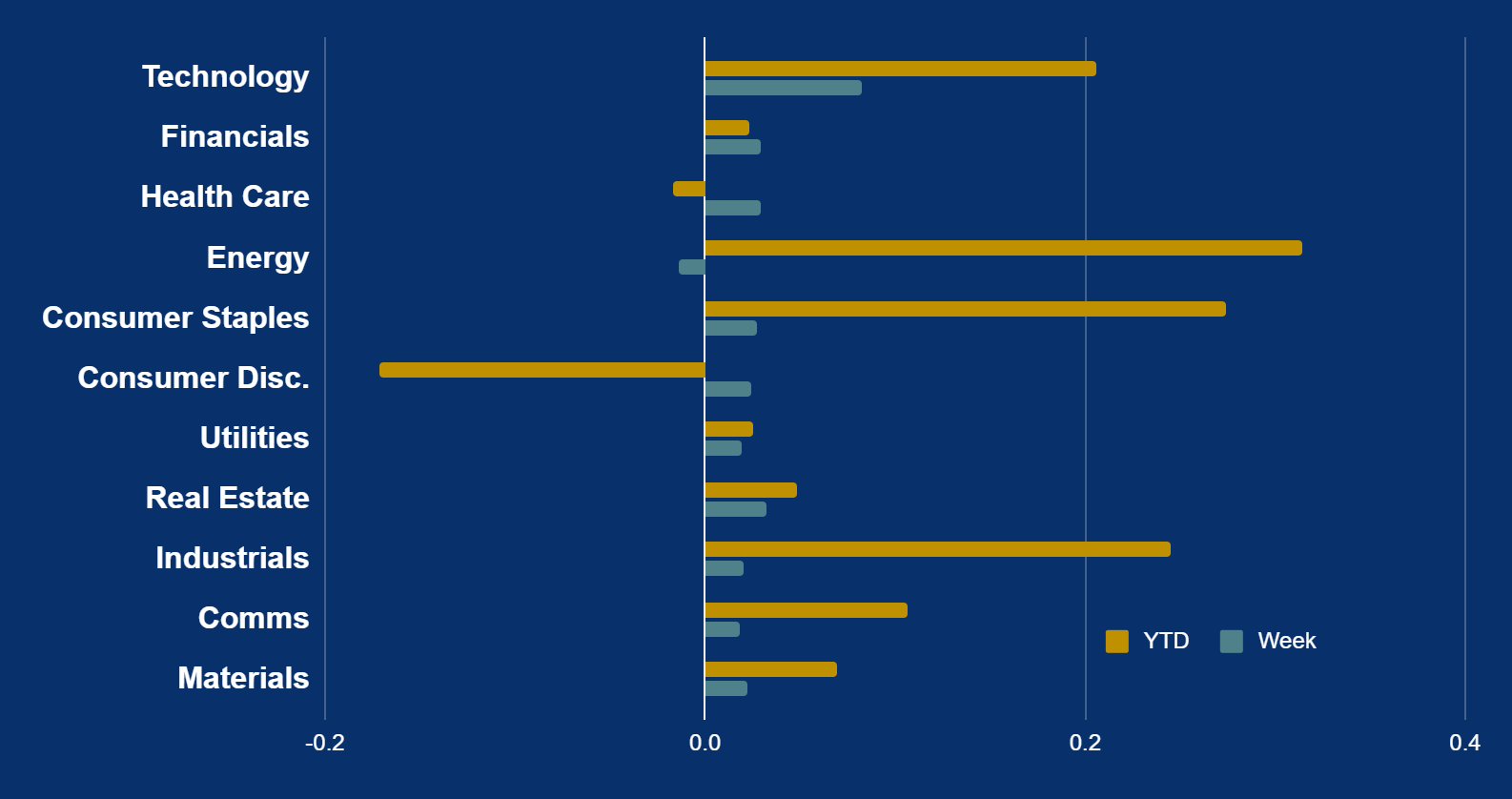

SECTORS

European markets surged this week, led by Technology (8.25%) as AI infrastructure momentum and Nokia’s new partnerships fueled gains. Real Estate (3.23%) and Financials (2.95%) rose as investors anticipated ECB monetary easing despite persistent inflation. Conversely, the Energy sector fell 1.37% as markets weighed the impact of the Middle East conflict on corporate margins, with pressure on TotalEnergies and Eni. While Industrials (2.06%) benefited from increased defense spending, consumer sectors remained resilient despite high energy prices. Overall, the STOXX Europe 600 climbed toward 625, testing highs not seen since the conflict began.