Note: None of the material or content contained herein constitutes investment advice. It is solely for educational and informational purposes. Past performance is not an indicator of future performance. Sources: Fiscal.ai, Google Finance, 2 May 2026.

THE VIDEO BRIEF

THE AUDIO BRIEF

THE RUNDOWN

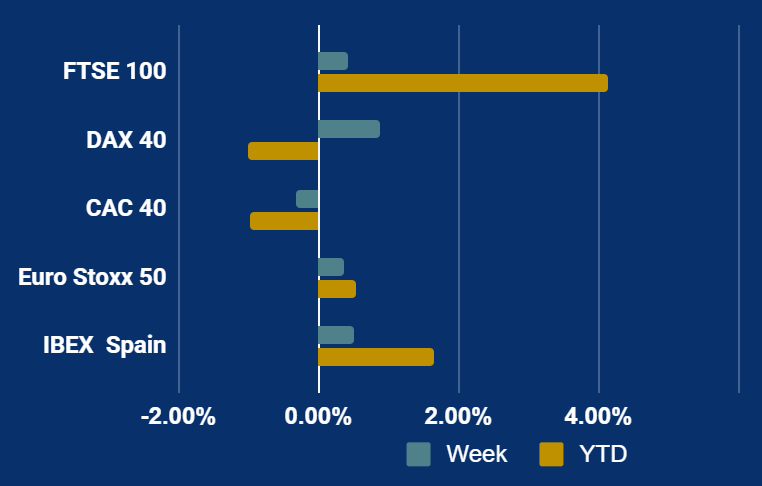

European markets showed mixed performance this past week.

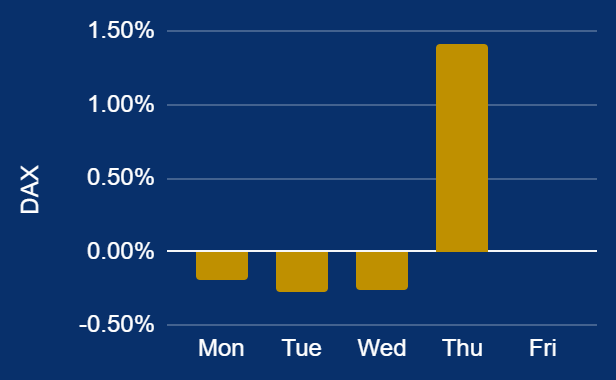

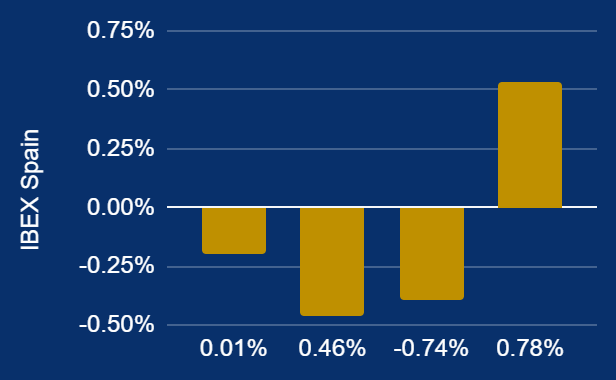

The DAX 40 rose 0.87%, bolstered by its high concentration of industrial and export-oriented firms benefiting from global trade. Spain's IBEX 35 gained 0.50% as its heavy weighting in the banking and energy sectors provided a hedge against broader volatility; notably, the Spanish energy sector surged 7.2% recently.

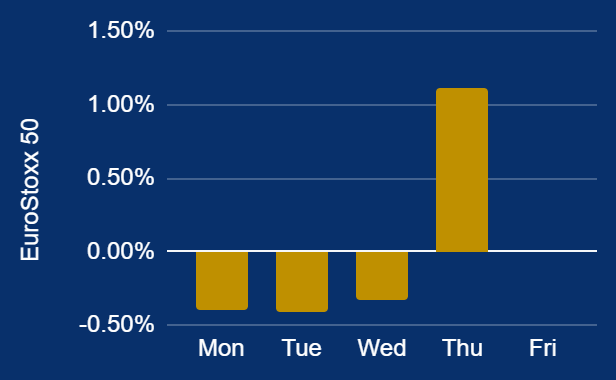

The Euro Stoxx 50 saw a modest 0.36% increase, reflecting balanced sentiment across blue-chip eurozone leaders.

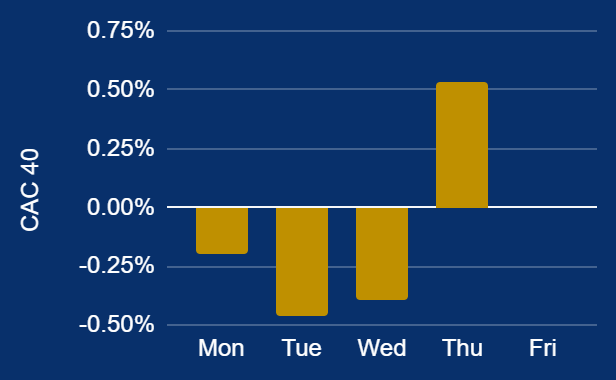

Conversely, the CAC 40 fell 0.33%. Despite strong earnings from luxury giants like Hermès, the French index was pressured by rising inflation concerns and geopolitical tensions in the Middle East, which historically impact its highly international constituents.

Investors remain focused on central bank policy as both the ECB and BoE recently held rates steady amid energy shock warnings.

MOVERS AND SHAKERS

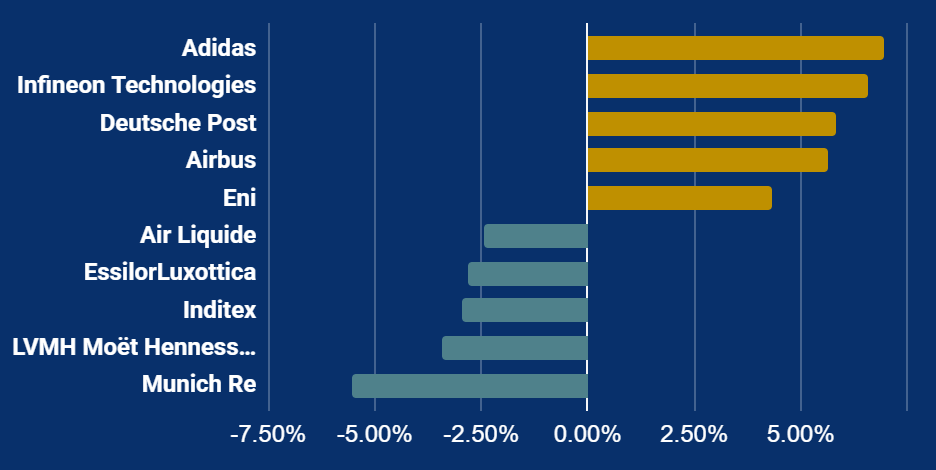

RISERS

Adidas is a sportswear giant that rose 6.97% after reporting stronger than expected first-quarter operating profit and robust double-digit revenue growth.

Infineon Technologies is a semiconductor manufacturer that gained 6.59% following robust quarterly results and increased optimism within the broader chip sector.

Deutsche Post is a global logistics group that climbed 5.84% after crushing analyst earnings expectations and demonstrating improved operational efficiency.

FALLERS

Munich Re is a global reinsurance company that fell 5.55% after reporting worse-than-expected quarterly profits caused by significant claims from natural disasters like hurricanes.

LVMH Moët Hennessy Louis Vuitton is a luxury goods conglomerate that dropped 3.43% due to slowing global demand and geopolitical instability impacting Middle Eastern sales.

Inditex is a major fashion retailer that fell 2.95% as part of a broader market downturn affecting consumer discretionary stocks amidst global economic uncertainty.

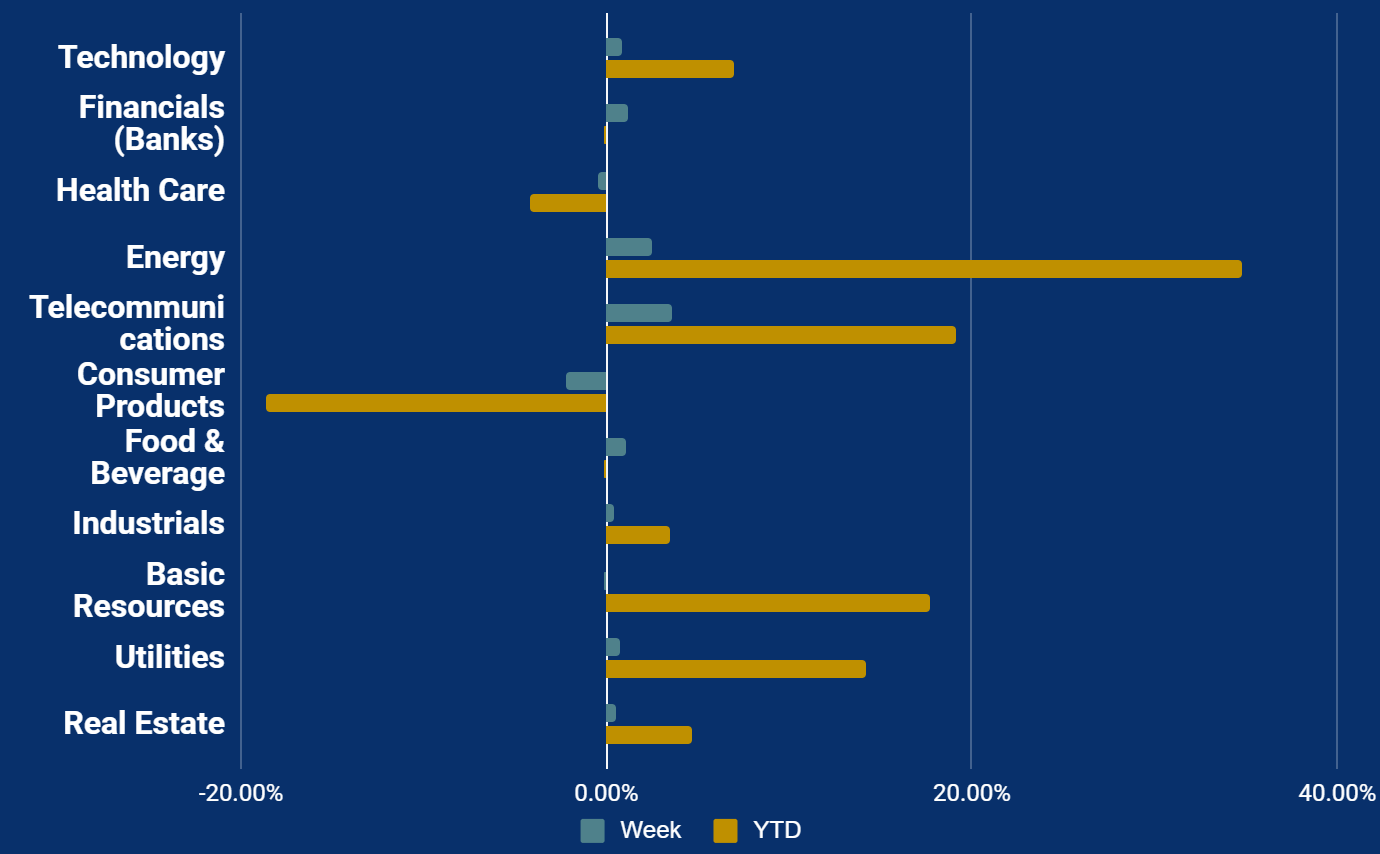

SECTORS

The week saw significant sector divergence driven by geopolitical and economic pressures. The energy sector rose 2.46% as supply fears intensified due to the closing of the Strait of Hormuz. Telecommunications led gains at 3.59% following reports of potential industry consolidation. Conversely, retail plummeted 2.66% and consumer products fell 2.19% as inflationary concerns and high interest rates dampened spending. Technology rose 0.85% supported by resilient corporate earnings, while health care slipped 0.51% as investors shifted toward cyclical assets. Overall, market sentiment remains cautious amid ongoing Middle East conflict and mixed corporate reporting.