Note: None of the material or content contained herein constitutes investment advice. It is solely for educational and informational purposes.

THE AUDIO BRIEF

THE RUNDOWN

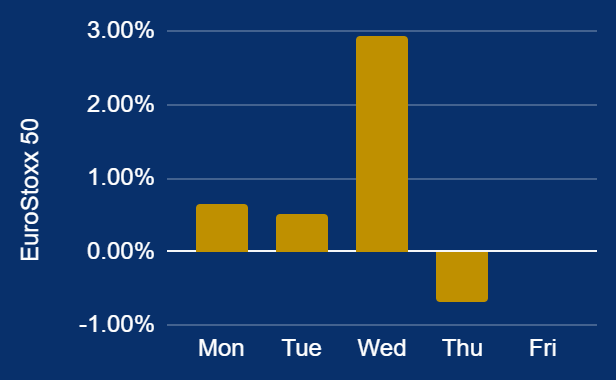

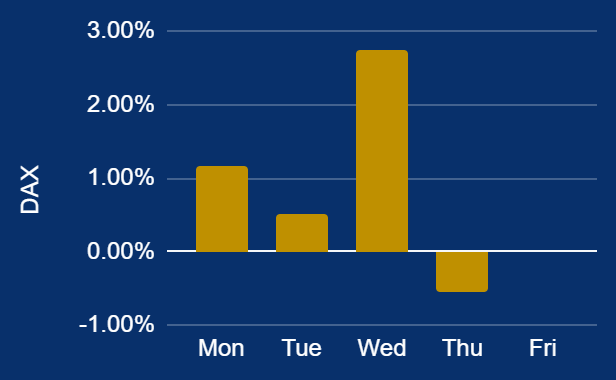

European markets saw gains this past week despite late-session volatility. The Euro Stoxx 50 rose 2.73%, while the DAX 40 gained 2.68%, supported by a recovery in industrial technology and defense sectors, even as a 3.3% slip in Deutsche Telekom weighed on Germany’s index.

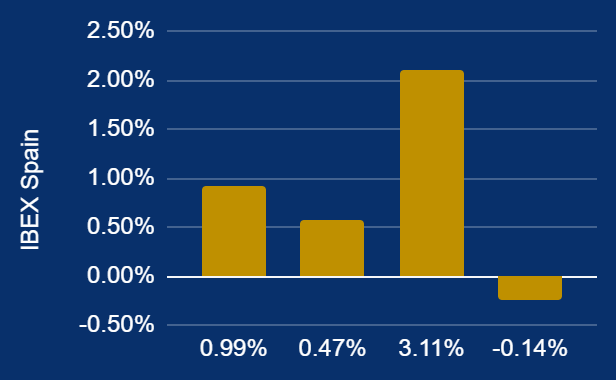

The IBEX Spain led with a 3.46% increase, buoyed by a strong banking sector that continues to benefit from interest rate normalization.

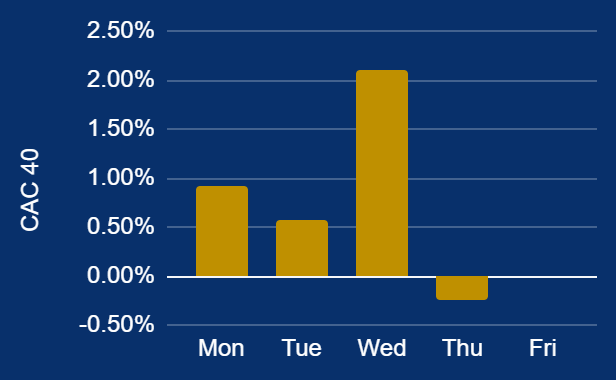

The CAC 40 increased 2.44%, driven by a resilient luxury sector and global demand for its aerospace components.

However, gains were tempered mid-week by geopolitical tensions in the Middle East and concerns over oil maritime traffic in the Strait of Hormuz, which triggered a pivot away from speculative tech assets and pressured financial institutions like BNP Paribas and UniCredit. Broad institutional buying and reduced geopolitical risk premiums earlier in the week provided the primary foundation for these positive returns.

MOVERS AND SHAKERS

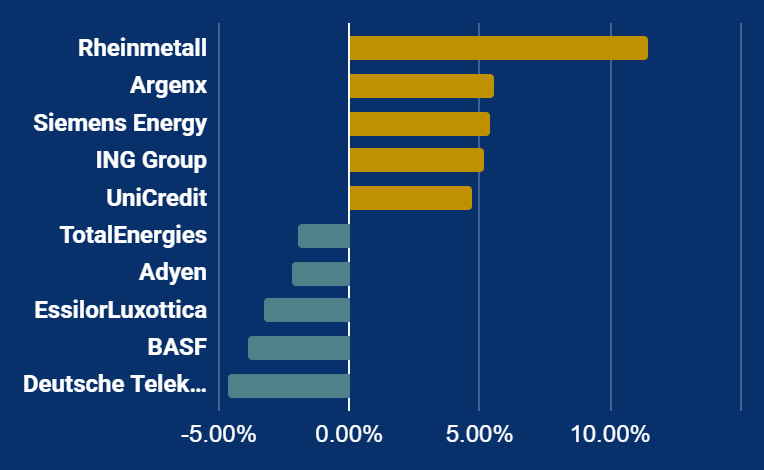

RISERS

Rheinmetall is a German defense manufacturer that rose 11.42% due to record military spending in Europe and a growing ammunition and combat vehicle order backlog.

Argenx is a global immunology company that gained 5.58% following strong product sales for its autoimmune treatments and positive updates to its drug pipeline.

Siemens Energy is an energy technology provider that climbed 5.42% after announcing a $1 billion investment to expand power grid infrastructure and manufacturing capacity.

FALLERS

Deutsche Telekom is a telecommunications provider that fell 4.62% after its 2025 earnings forecast and German business growth outlook missed analyst expectations.

BASF is a global chemical manufacturer that dropped 3.89% as its 2026 earnings outlook fell below estimates amid challenging demand and foreign exchange headwinds.

EssilorLuxottica is an eyewear and lens producer that declined 3.26% due to rising competitive risks from technology companies and a patent infringement lawsuit.

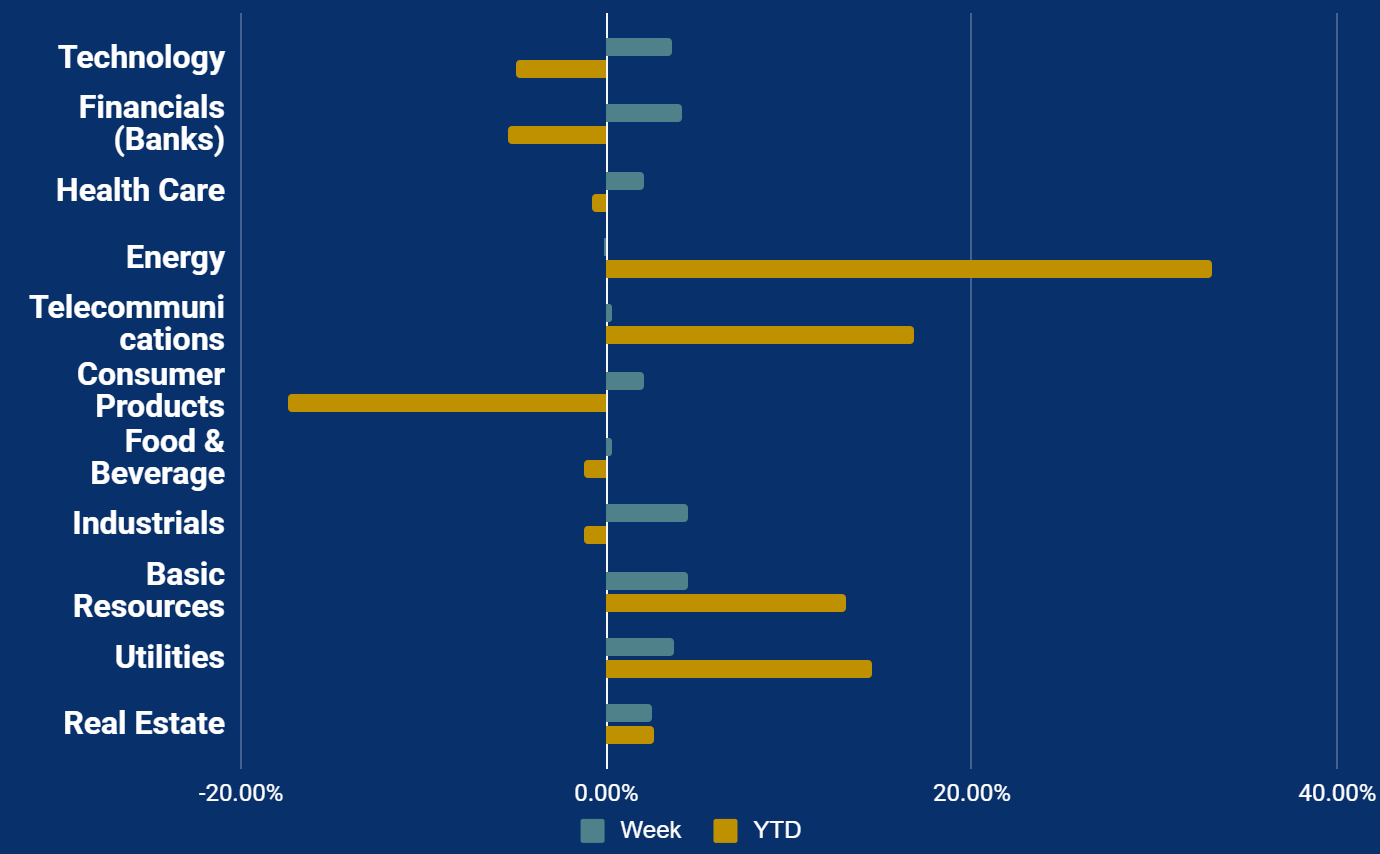

SECTORS

Sectors rebounded last week as hopes for de-escalation in the Middle East fueled a relief rally. Industrials led gains, rising 4.49%, while Basic Resources followed at 4.47% as investors rotated into lagging sectors. Technology rose 3.57%, benefiting from continued AI infrastructure buildout. Financials climbed 4.12% despite earlier credit concerns. Conversely, Energy fell 0.11% as news of a potential deal to reopen the Strait of Hormuz caused oil prices to ease from recent peaks. Utilities and Health Care rose 3.69% and 2.10%, respectively, as investors sought defensive positioning amid ongoing geopolitical uncertainty and sticky inflation.